RSS

RSSLog normal distribution

Where do you meet this distribution?

- Finance, Economics : Change of stock price

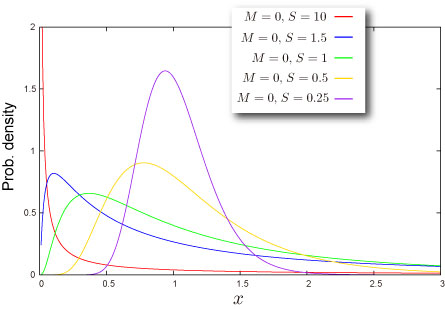

Shape of Distribution

Basic Properties

- Two parameters

are required (How can you get these).

- Continuous distribution defined on semi-bounded range

- This distribution is always asymmetric.

Probability

- Cumulative distribution function

where

is cumulative distribution function of standard normal distribution.

- Probability density function

where

is probability density function of standard normal distribution.

- How to compute these on Excel.

1 2 3 4 5 6

7

A B Data Description 0.5 Value for which you want the distribution 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMDIST(A2,A3,A4,TRUE) Cumulative distribution function for the terms above =NTLOGNORMDIST(A2,A3,A4,FALSE) Probability density function for the terms above

- Function reference : NTLOGNORMDIST

=\Phi\left(\frac{\ln x-M}{S}\right)")

=\frac{1}{Sx}\phi\left(\frac{\ln x-M}{S}\right)")

Quantile

- Inverse function of cumulative distribution function

where

- How to compute this on Excel.

1 2 3 4 5 6

A B Data Description 0.7 Probability associated with the distribution 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMINV(A2,A3,A4) Inverse of the cumulative distribution function for the terms above

![F^{-1}(P)=\exp\left[S\Phi^{-1}(P)+M\right]](http://s0.wp.com/latex.php?latex=F%5E%7B-1%7D%28P%29%3D%5Cexp%5Cleft%5BS%5CPhi%5E%7B-1%7D%28P%29%2BM%5Cright%5D&bg=T&fg=000000&s=0 "F^{-1}(P)=\exp\left[S\Phi^{-1}(P)+M\right]")

Characteristics

Mean – Where is the “center” of the distribution? (Definition)

- Mean of the distribution is given as

where

- How to compute this on Excel

1 2 3 4 5 A B Data Description 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMMEAN(A2,A3) Mean of the distribution for the terms above - Function reference : NTLOGNORMMEAN

,\;\omega=\exp(S^2)")

Standard Deviation – How wide does the distribution spread? (Definition)

- Variance of the distribution is given as

where

Standard Deviation is a positive square root of Variance.

- How to compute this on Excel

1 2 3 4 5

A B Data Description 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMSTDEV(A2,A3) Standard deviation of the distribution for the terms above - Function reference : NTLOGNORMSTDEV

")

Skewness – Which side is the distribution distorted into? (Definition)

- Skewness of the distribution is given as

where

- How to compute this on Excel

1 2 3 4 5 A B Data Description 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMSKEW(A2,A3) Skewness of the distribution for the terms above - Function reference : NTLOGNORMSKEW

\sqrt{\omega-1}")

")

Kurtosis – Sharp or Dull, consequently Fat Tail or Thin Tail (Definition)

- Kurtosis of the distribution is given as

where

- How to compute this on Excel

1 2 3 4 5 A B Data Description 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTLOGNORMKURT(A2,A3) Kurtosis of the distribution for the terms above - Function reference : NTLOGNORMKURT

Random Numbers

- Random number x is generated by inverse function method, which is for uniform random U,

where

- How to generate random numbers on Excel.

1 2 3 4 5

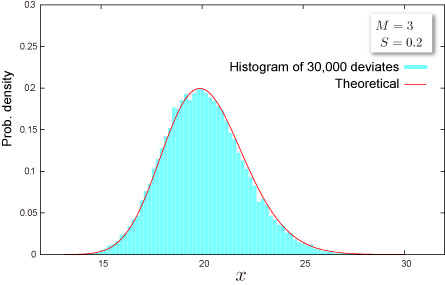

A B Data Description 0.1 Value of parameter M 2 Value of parameter S Formula Description (Result) =NTRANDLOGNORM(100,A2,A3,0) 100 log normal deviates based on Mersenne-Twister algorithm for which the parameters above Note The formula in the example must be entered as an array formula. After copying the example to a blank worksheet, select the range A7:A106 starting with the formula cell. Press F2, and then press CTRL+SHIFT+ENTER.

- Function reference : NTRANDLOGNORM

![x=\exp\left[S\Phi^{-1}(U)+M\right]](http://s0.wp.com/latex.php?latex=x%3D%5Cexp%5Cleft%5BS%5CPhi%5E%7B-1%7D%28U%29%2BM%5Cright%5D&bg=T&fg=000000&s=0 "x=\exp\left[S\Phi^{-1}(U)+M\right]")

NtRand Functions

- If you already have parameters of the distribution

- Generating random numbers based on Mersenne Twister algorithm: NTRANDLOGNORM

- Computing probability : NTLOGNORMDIST

- Computing mean : NTLOGNORMMEAN

- Computing standard deviation : NTLOGNORMSTDEV

- Computing skewness : NTLOGNORMSKEW

- Computing kurtosis : NTLOGNORMKURT

- Computing moments above at once : NTLOGNORMMOM

- If you know mean and standard deviation of the distribution

- Estimating parameters of the distribution:NTLOGNORMPARAM

Reference

- Wolfram Mathworld – Log Normal Distribution

- Wikipedia – Log-normal distribution

- Statistics Online Computational Resource